Quickstart¶

This guide will help you get up-and-running with crvUSDsim.

First, make sure that:

crvUSDsim is installed

crvUSDsim is up-to-date

Hello world¶

Before digging into more interesting examples, let’s check the installed package can run without issues. In the console, run:

$ python3 -m crvusdsim

[INFO][11:29:54][crvusdsim.pipelines.simple]-92751: Simulating mode: rate

[INFO][11:29:57][curvesim.price_data.sources]-92751: Fetching CoinGecko price data...

[INFO][11:30:08][curvesim.price_data.sources]-92751: Fetching CoinGecko price data...

[INFO][11:30:08][curvesim.price_data.sources]-92751: Fetching CoinGecko price data...

[INFO][11:30:08][curvesim.price_data.sources]-92751: Fetching CoinGecko price data...

[INFO][11:30:09][curvesim.price_data.sources]-92751: Fetching CoinGecko price data...

[INFO][11:30:16][crvusdsim.templates.Strategy]-92883: [Curve.fi Stablecoin wstETH] Simulating with {'rate0': 0.15}

[INFO][11:30:16][crvusdsim.templates.Strategy]-92880: [Curve.fi Stablecoin wstETH] Simulating with {'rate0': 0.1}

[INFO][11:30:16][crvusdsim.templates.Strategy]-92877: [Curve.fi Stablecoin wstETH] Simulating with {'rate0': 0.05}

Elapsed time: 28.6576099395752

Fetch a series of objects from Curve stablecoin wstETH market¶

Use collateral assets symbol, or if you know the address of the collateral asset, you can easily start interacting with it. crvUSDsim allows you to introspect on the market’s state and use its functions without submitting actual transactions on chain.

Begin by importing the crvUSDsim module:

>>> import crvusdsim

Let’s retrieve a series of objects from Curve stablecoin wstETH market:

>>> collateral_name = "wstETH" # or collateral_address "0x37417b2238aa52d0dd2d6252d989e728e8f706e4"

>>> (pool, controller, collateral_token, stablecoin, aggregator, stableswap_pools, peg_keepers, policy, factory)

>>> = crvusdsim.pool.get(market_name)

Now, we have a series of wstETH market objects:

pool:SimLLAMMAPoolobjectcontroller:SimControllerobjectcollateral_token:ERC20objectstablecoin:StableCoinobjectaggregator:AggregateStablePriceobjectstableswap_pools: List[CurveStableSwapPool]peg_keepers: List[PegKeeper]policy:MonetaryPolicyobjectfactory:ControllerFactoryobject

Its state is pulled from daily snapshots of the Curve volume subgraph’s crvusd module. From this object we can retrieve state information and see the result of pool operations such as swaps or adding liquidity.

The pool interface adheres closely to the live smart contract’s, so if you are familiar with the vyper contract, you should feel at home.

For example, to check various data about the pool:

>>> pool.name

'Curve.fi Stablecoin wstETH'

>>> pool.coin_names

['wstETH', 'crvUSD']

>>> pool.A

100

>>> controller.loan_discount

90000000000000000

>>> controller.liquidation_discount

60000000000000000

Do some trade on pool, trade function will use ARBITRAGUR as trader’s address, and mint token to ARBITRAGUR automatically:

>>> dx = 10**18

>>> pool.trade(0, 1, dx) # dx, dy, fees

(1000000000000000000, 445225238462727, 6000000000000000)

If you want to dig into the pulled data that was used to construct the pool:

>>> pool.metadata

{'llamma_params': {'name': 'Curve.fi Stablecoin wstETH',

'address': '0x37417b2238aa52d0dd2d6252d989e728e8f706e4',

'A': '100',

'rate': '4010591623',

'rate_mul': '1024868101325770634',

'fee': '0.006',

'admin_fee': '0.000000000000000001',

'BASE_PRICE': '2117.144587304125327462',

'active_band': '-12',

'min_band': '-14',

'max_band': '1034',

'oracle_price': '2373.921229194305616293',

'collateral_address': '0x7f39c581f595b53c5cb19bd0b3f8da6c935e2ca0',

'collateral_precision': '18',

'collateral_name': 'wstETH',

'collateral_symbol': 'wstETH',

'bands_x': defaultdict(int,

...

'addresses': ['0xf939e0a03fb07f59a73314e73794be0e57ac1b4e', '0x7f39C581F595B53c5cb19bD0b3f8dA6c935E2Ca0'],

'decimals': [18, 18]},

'address': '0x37417b2238aa52d0dd2d6252d989e728e8f706e4',

'chain': 'mainnet'}

If you want to get objects with bands data or users’ loan data, simply use bands_data parameter, the valid value is pool or controller:

# get pool with `bands_x` and `bands_y` data

>>> (pool, controller, ...) = crvusdsim.pool.get(market_name, bands_data="pool")

>>> sum(pool.bands_x.values())

0

>>> sum(pool.bands_y.values())

40106052164494685140992

# get pool with `bands_x`, `bands_y`, `user_shares` data

# and controller with `loan`, `loans`, `loan_ix` data

>>> (pool, controller, ...) = crvusdsim.pool.get(market_name, bands_data="controller")

>>> len(pool.user_shares)

392

>>> len(controller.loan)

392

>>> user0 = controller.loans[1] # user address

>>> loan0 = controller.loan[user0] # :class:Loan

>>> (loan0.initial_debt, loan0.initial_collateral, loan0.rate_mul, loan0.timestamp)

(9779961749290509154648064, 6785745612366175797248, 1000000000000000000, 1700712599)

Run an arbitrage simulation for a proposed parameter¶

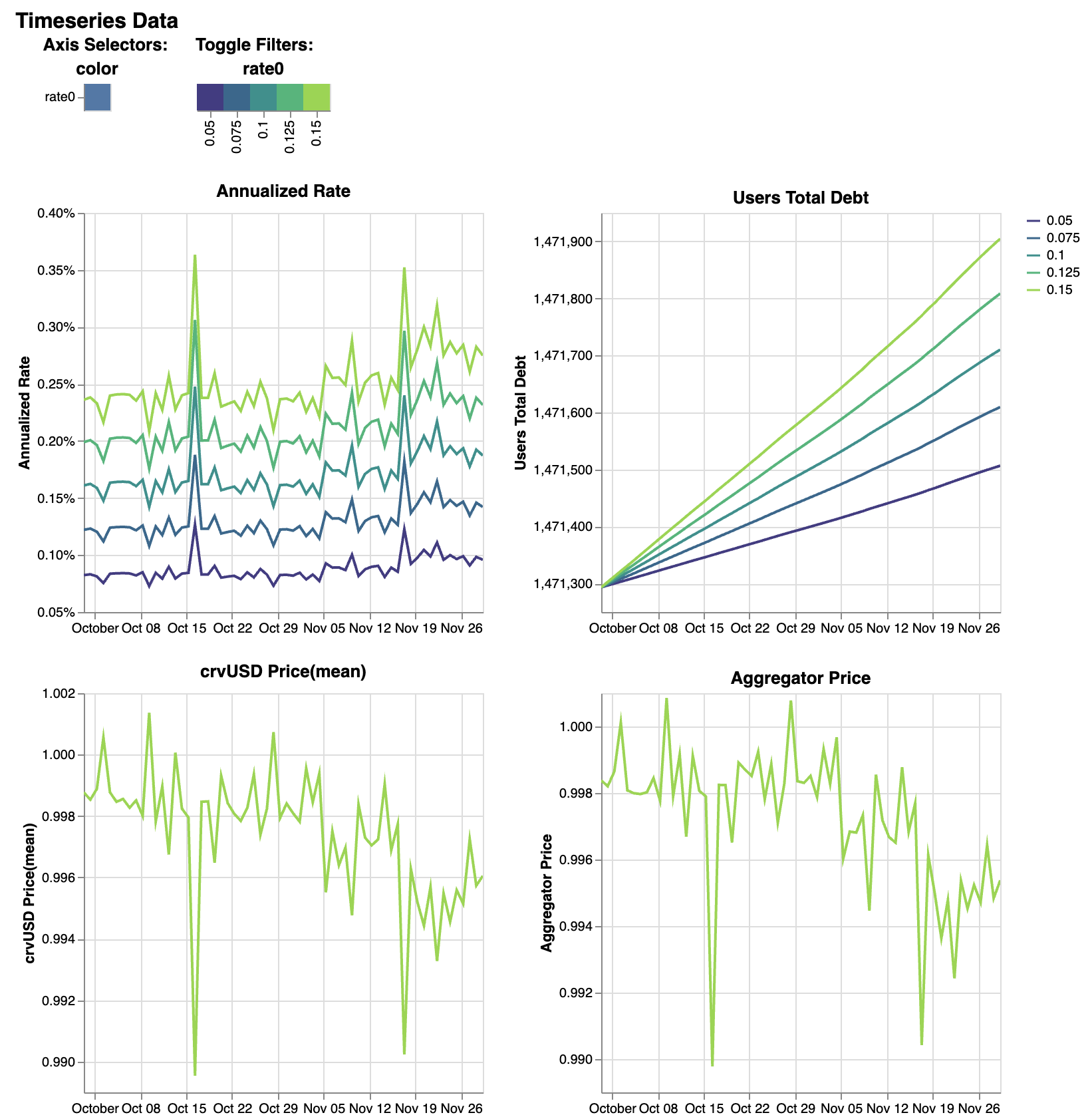

Rate simulations to see results of varying rate0 parameters in MonetaryPolicy:

>>> import crvusdsim

>>> res = crvusdsim.autosim(pool="wstETH", sim_mode="rate", rate0=[0.05, 0.075, 0.10, 0.125, 0.15])

[INFO][10:02:42][crvusdsim.pipelines.simple]-84886: Simulating mode: rate

[INFO][10:02:50][curvesim.price_data.sources]-84886: Fetching CoinGecko price data...

[INFO][10:03:51][curvesim.price_data.sources]-84886: Fetching CoinGecko price data...

[INFO][10:03:52][curvesim.price_data.sources]-84886: Fetching CoinGecko price data...

[INFO][10:05:44][curvesim.price_data.sources]-84886: Fetching CoinGecko price data...

[INFO][10:07:22][curvesim.price_data.sources]-84886: Fetching CoinGecko price data...

[INFO][10:07:32][crvusdsim.templates.Strategy]-84936: [Curve.fi Stablecoin wstETH] Simulating with {'rate0': 0.05}

[INFO][10:07:32][crvusdsim.templates.Strategy]-84937: [Curve.fi Stablecoin wstETH] Simulating with {'rate0': 0.125}

[INFO][10:07:32][crvusdsim.templates.Strategy]-84935: [Curve.fi Stablecoin wstETH] Simulating with {'rate0': 0.075}

[INFO][10:07:32][crvusdsim.templates.Strategy]-84934: [Curve.fi Stablecoin wstETH] Simulating with {'rate0': 0.1}

[INFO][10:07:33][crvusdsim.templates.Strategy]-84938: [Curve.fi Stablecoin wstETH] Simulating with {'rate0': 0.15}

>>> res.summary()

metric annualized_rate users_debt crvusd_price agg_price

stat mean mean mean mean

0 0.000868 1.471397e+06 0.997661 0.997426

1 0.001287 1.471446e+06 0.997661 0.997426

2 0.001697 1.471495e+06 0.997661 0.997426

3 0.002097 1.471543e+06 0.997661 0.997426

4 0.002490 1.471589e+06 0.997661 0.997426

>>> res.summary(full=True)

rate0 annualized_rate mean users_debt mean crvusd_price mean agg_price mean

0 0.050 0.000868 1.471397e+06 0.997661 0.997426

1 0.075 0.001287 1.471446e+06 0.997661 0.997426

2 0.100 0.001697 1.471495e+06 0.997661 0.997426

3 0.125 0.002097 1.471543e+06 0.997661 0.997426

4 0.150 0.002490 1.471589e+06 0.997661 0.997426

>>> res.data()

run timestamp annualized_rate users_debt crvusd_price agg_price

0 0 2023-09-29 23:30:00+00:00 0.000824 1.471293e+06 0.998771 0.998381

1 0 2023-09-29 23:38:34+00:00 0.000824 1.471293e+06 0.998771 0.998381

2 0 2023-09-29 23:47:08+00:00 0.000824 1.471293e+06 0.998771 0.998381

3 0 2023-09-29 23:55:42+00:00 0.000824 1.471293e+06 0.998771 0.998381

4 0 2023-09-30 00:04:17+00:00 0.000824 1.471293e+06 0.998771 0.998381

... ... ... ... ... ... ...

51240 4 2023-11-29 22:55:42+00:00 0.002746 1.471905e+06 0.996052 0.995404

51241 4 2023-11-29 23:04:17+00:00 0.002746 1.471905e+06 0.996052 0.995404

51242 4 2023-11-29 23:12:51+00:00 0.002746 1.471905e+06 0.996052 0.995404

51243 4 2023-11-29 23:21:25+00:00 0.002746 1.471905e+06 0.996052 0.995404

51244 4 2023-11-29 23:30:00+00:00 0.002750 1.471905e+06 0.996052 0.995373

51245 rows x 6 columns

>>> res.data(full=True)

rate0 run timestamp annualized_rate users_debt crvusd_price agg_price

0 0.05 0 2023-09-29 23:30:00+00:00 0.000824 1.471293e+06 0.998771 0.998381

1 0.05 0 2023-09-29 23:38:34+00:00 0.000824 1.471293e+06 0.998771 0.998381

2 0.05 0 2023-09-29 23:47:08+00:00 0.000824 1.471293e+06 0.998771 0.998381

3 0.05 0 2023-09-29 23:55:42+00:00 0.000824 1.471293e+06 0.998771 0.998381

4 0.05 0 2023-09-30 00:04:17+00:00 0.000824 1.471293e+06 0.998771 0.998381

... ... ... ... ... ... ... ...

51240 0.15 4 2023-11-29 22:55:42+00:00 0.002746 1.471905e+06 0.996052 0.995404

51241 0.15 4 2023-11-29 23:04:17+00:00 0.002746 1.471905e+06 0.996052 0.995404

51242 0.15 4 2023-11-29 23:12:51+00:00 0.002746 1.471905e+06 0.996052 0.995404

51243 0.15 4 2023-11-29 23:21:25+00:00 0.002746 1.471905e+06 0.996052 0.995404

51244 0.15 4 2023-11-29 23:30:00+00:00 0.002750 1.471905e+06 0.996052 0.995373

51245 rows x 7 columns

Tuning a pool parameter, such as the amplification coefficient A.:

>>> import crvusdsim

>>> market_name = "wstETH"

>>> res = crvusdsim.autosim(pool="wstETH", sim_mode="pool", A=100)

[INFO][14:57:58][crvusdsim.pipelines.simple]-82656: Simulating mode: pool

[INFO][14:58:00][curvesim.price_data.sources]-82656: Fetching CoinGecko price data...

[INFO][14:58:05][crvusdsim.templates.Strategy]-82730: [Curve.fi Stablecoin wstETH] Simulating with {'A': 100}

Likely you will want to see the impact over a range of A values. The A and fee parameters

will accept either a integer or iterables of integers; note fee values are in units of basis points

multiplied by 10**18.:

>>> res = crvusdsim.autosim(pool="wstETH", sim_mode="pool", A=[50, 60, 80, 100], fee=[6 * 10**15, 10 * 10**15])

[INFO][11:08:46][crvusdsim.pipelines.simple]-33804: Simulating mode: pool

[INFO][11:09:10][curvesim.price_data.sources]-33804: Fetching CoinGecko price data...

[INFO][11:09:44][crvusdsim.templates.Strategy]-33869: [Curve.fi Stablecoin wstETH] Simulating with {'A': 50, 'fee': 6000000000000000}

[INFO][11:09:44][crvusdsim.templates.Strategy]-33870: [Curve.fi Stablecoin wstETH] Simulating with {'A': 50, 'fee': 10000000000000000}

[INFO][11:09:44][crvusdsim.templates.Strategy]-33876: [Curve.fi Stablecoin wstETH] Simulating with {'A': 60, 'fee': 10000000000000000}

[INFO][11:09:44][crvusdsim.templates.Strategy]-33875: [Curve.fi Stablecoin wstETH] Simulating with {'A': 100, 'fee': 6000000000000000}

[INFO][11:09:44][crvusdsim.templates.Strategy]-33873: [Curve.fi Stablecoin wstETH] Simulating with {'A': 80, 'fee': 6000000000000000}

[INFO][11:09:44][crvusdsim.templates.Strategy]-33871: [Curve.fi Stablecoin wstETH] Simulating with {'A': 60, 'fee': 6000000000000000}

[INFO][11:09:44][crvusdsim.templates.Strategy]-33872: [Curve.fi Stablecoin wstETH] Simulating with {'A': 80, 'fee': 10000000000000000}

[INFO][11:09:45][crvusdsim.templates.Strategy]-33874: [Curve.fi Stablecoin wstETH] Simulating with {'A': 100, 'fee': 10000000000000000}

>>> res.summary()

metric pool_value loss_value pool_volume arb_profit pool_fees

stat annualized_returns annualized_arb_profits sum sum sum

0 0.569850 0.031372 5.521713e+09 1.017937e+07 7.298168e+07

1 0.533898 0.025810 4.358760e+09 8.319915e+06 9.826156e+07

2 0.573620 0.029282 5.347932e+09 9.473498e+06 7.089184e+07

3 0.553401 0.022987 3.987458e+09 7.478085e+06 9.083868e+07

4 0.571523 0.029660 5.389022e+09 9.611733e+06 7.140822e+07

5 0.529070 0.027319 4.241904e+09 8.805979e+06 9.597500e+07

6 0.569426 0.030513 5.393248e+09 9.903716e+06 7.147705e+07

7 0.554593 0.022389 4.017923e+09 7.283106e+06 9.152026e+07

>>> res.summary(full=True)

A Fee pool_value annualized_returns loss_value annualized_arb_profits pool_volume sum arb_profit sum pool_fees sum

0 50 0.006 0.569850 0.031372 5.521713e+09 1.017937e+07 7.298168e+07

1 50 0.010 0.533898 0.025810 4.358760e+09 8.319915e+06 9.826156e+07

2 60 0.006 0.573620 0.029282 5.347932e+09 9.473498e+06 7.089184e+07

3 60 0.010 0.553401 0.022987 3.987458e+09 7.478085e+06 9.083868e+07

4 80 0.006 0.571523 0.029660 5.389022e+09 9.611733e+06 7.140822e+07

5 80 0.010 0.529070 0.027319 4.241904e+09 8.805979e+06 9.597500e+07

6 100 0.006 0.569426 0.030513 5.393248e+09 9.903716e+06 7.147705e+07

7 100 0.010 0.554593 0.022389 4.017923e+09 7.283106e+06 9.152026e+07

>>> res.data()

run timestamp pool_value loss_value pool_volume arb_profit pool_fees

0 0 2023-09-29 23:30:00+00:00 1.879406e+09 0.000000 0.0 0.0 0.0

1 0 2023-09-29 23:38:34+00:00 1.879531e+09 0.000000 0.0 0.0 0.0

2 0 2023-09-29 23:47:08+00:00 1.879656e+09 0.000000 0.0 0.0 0.0

3 0 2023-09-29 23:55:42+00:00 1.879781e+09 0.000000 0.0 0.0 0.0

4 0 2023-09-30 00:04:17+00:00 1.879906e+09 0.000000 0.0 0.0 0.0

... ... ... ... ... ... ... ...

81987 7 2023-11-29 22:55:42+00:00 2.034973e+09 0.003707 0.0 0.0 0.0

81988 7 2023-11-29 23:04:17+00:00 2.034973e+09 0.003707 0.0 0.0 0.0

81989 7 2023-11-29 23:12:51+00:00 2.034973e+09 0.003707 0.0 0.0 0.0

81990 7 2023-11-29 23:21:25+00:00 2.034973e+09 0.003707 0.0 0.0 0.0

81991 7 2023-11-29 23:30:00+00:00 2.034973e+09 0.003707 0.0 0.0 0.0

81992 rows × 7 columns

>>> res.data(full=True)

A Fee run timestamp pool_value loss_value pool_volume arb_profit pool_fees

0 50 0.006 0 2023-09-29 23:30:00+00:00 1.879406e+09 0.000000 0.0 0.0 0.0

1 50 0.006 0 2023-09-29 23:38:34+00:00 1.879531e+09 0.000000 0.0 0.0 0.0

2 50 0.006 0 2023-09-29 23:47:08+00:00 1.879656e+09 0.000000 0.0 0.0 0.0

3 50 0.006 0 2023-09-29 23:55:42+00:00 1.879781e+09 0.000000 0.0 0.0 0.0

4 50 0.006 0 2023-09-30 00:04:17+00:00 1.879906e+09 0.000000 0.0 0.0 0.0

... ... ... ... ... ... ... ... ... ...

81987 100 0.010 7 2023-11-29 22:55:42+00:00 2.034973e+09 0.003707 0.0 0.0 0.0

81988 100 0.010 7 2023-11-29 23:04:17+00:00 2.034973e+09 0.003707 0.0 0.0 0.0

81989 100 0.010 7 2023-11-29 23:12:51+00:00 2.034973e+09 0.003707 0.0 0.0 0.0

81990 100 0.010 7 2023-11-29 23:21:25+00:00 2.034973e+09 0.003707 0.0 0.0 0.0

81991 100 0.010 7 2023-11-29 23:30:00+00:00 2.034973e+09 0.003707 0.0 0.0 0.0

81992 rows x 9 columns

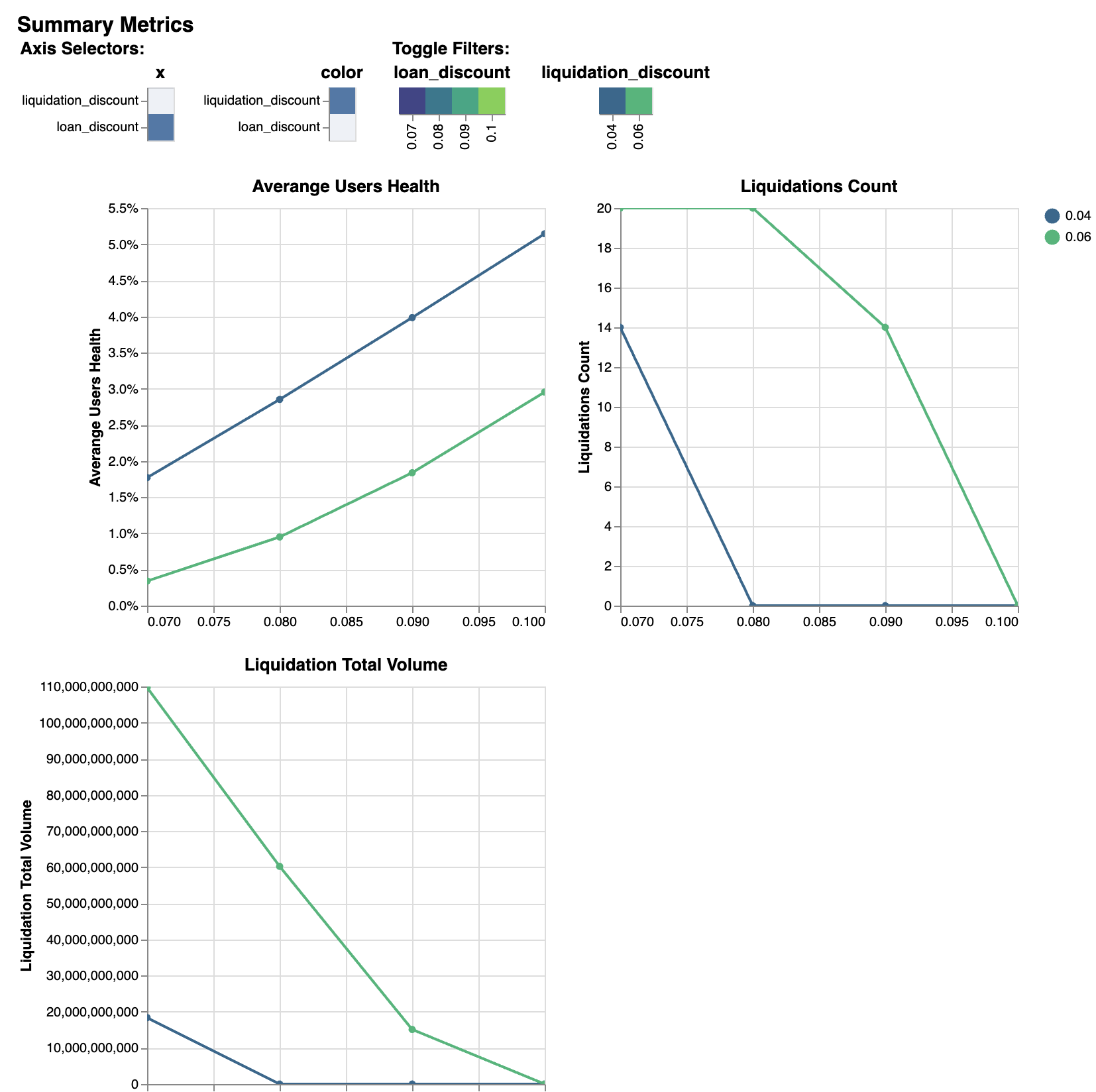

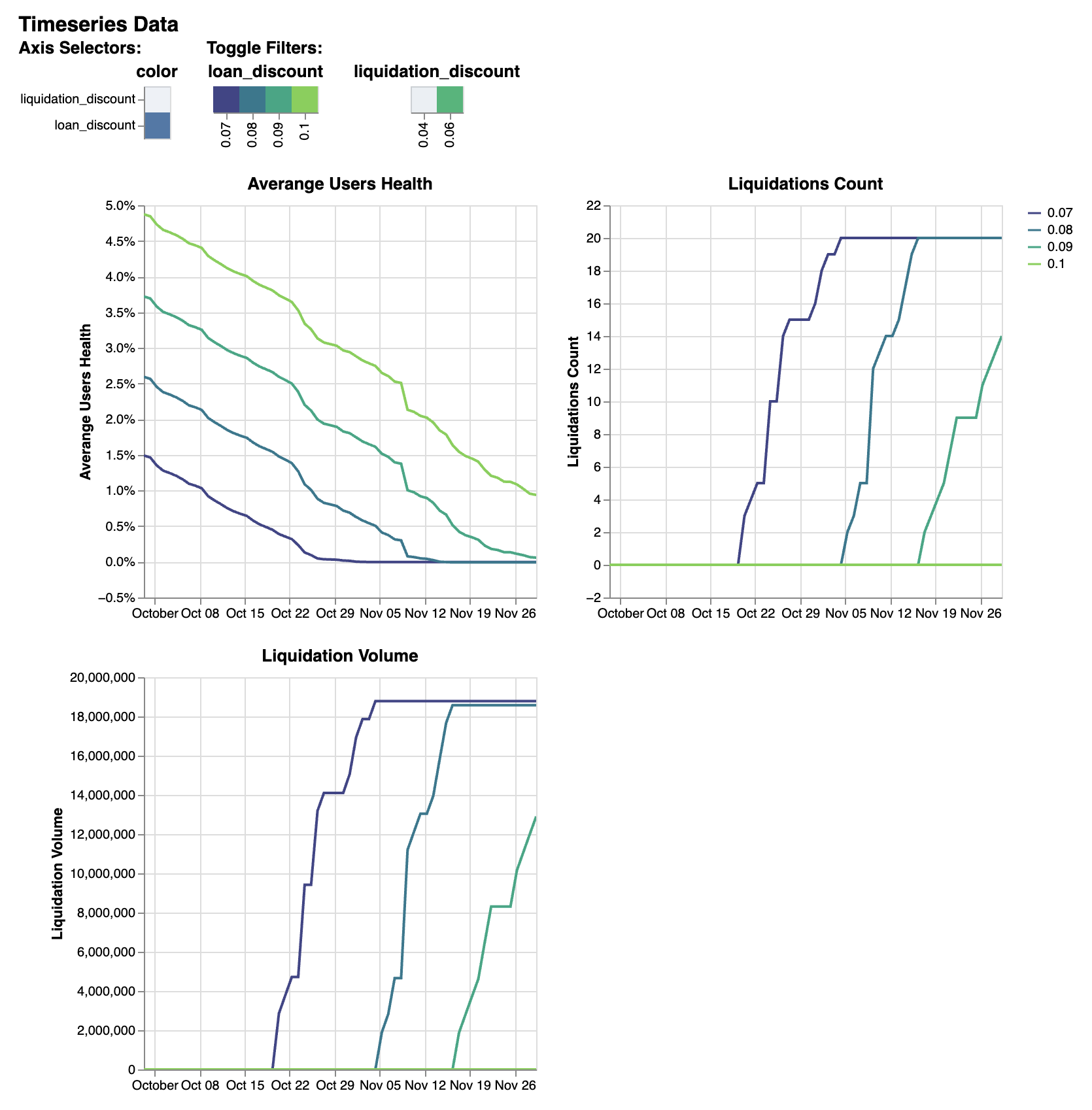

To simlate controller’s parameters, such as loan_discount and liquidation_discount, use sim_mode="controller":

>>> res = crvusdsim.autosim(pool="wstETH", sim_mode="controller",

>>> loan_discount=[int(0.07 * 10**18), int(0.08 * 10**18), int(0.09 * 10**18), int(0.10 * 10**18)],

>>> liquidation_discount=[int(0.04 * 10**18), int(0.06 * 10**18)])

[INFO][14:56:36][crvusdsim.pipelines.simple]-7441: Simulating mode: controller

[INFO][14:56:36][curvesim.price_data.sources]-7441: Fetching CoinGecko price data...

[INFO][14:57:15][crvusdsim.templates.Strategy]-41713: [Curve.fi Stablecoin wstETH] Simulating with {'loan_discount': 80000000000000000, 'liquidation_discount': 60000000000000000}

[INFO][14:57:16][crvusdsim.templates.Strategy]-41710: [Curve.fi Stablecoin wstETH] Simulating with {'loan_discount': 70000000000000008, 'liquidation_discount': 40000000000000000}

[INFO][14:57:16][crvusdsim.templates.Strategy]-41712: [Curve.fi Stablecoin wstETH] Simulating with {'loan_discount': 80000000000000000, 'liquidation_discount': 40000000000000000}

[INFO][14:57:16][crvusdsim.templates.Strategy]-41714: [Curve.fi Stablecoin wstETH] Simulating with {'loan_discount': 90000000000000000, 'liquidation_discount': 40000000000000000}

[INFO][14:57:16][crvusdsim.templates.Strategy]-41711: [Curve.fi Stablecoin wstETH] Simulating with {'loan_discount': 70000000000000008, 'liquidation_discount': 60000000000000000}

[INFO][14:57:16][crvusdsim.templates.Strategy]-41716: [Curve.fi Stablecoin wstETH] Simulating with {'loan_discount': 90000000000000000, 'liquidation_discount': 60000000000000000}

[INFO][14:57:16][crvusdsim.templates.Strategy]-41717: [Curve.fi Stablecoin wstETH] Simulating with {'loan_discount': 100000000000000000, 'liquidation_discount': 60000000000000000}

[INFO][14:57:16][crvusdsim.templates.Strategy]-41715: [Curve.fi Stablecoin wstETH] Simulating with {'loan_discount': 100000000000000000, 'liquidation_discount': 40000000000000000}

>>> res.summary()

metric averange_user_health liquidations_count liquidation_volume

stat mean max sum

0 0.017705 14.0 1.835876e+10

1 0.003404 20.0 1.097029e+11

2 0.028522 0.0 0.000000e+00

3 0.009494 20.0 6.023163e+10

4 0.039849 0.0 0.000000e+00

5 0.018384 14.0 1.510470e+10

6 0.051448 0.0 0.000000e+00

7 0.029543 0.0 0.000000e+00

>>> res.summary(full=True)

loan_discount liquidation_discount averange_user_health mean liquidations_count max liquidation_volume sum

0 0.07 0.04 0.017705 14.0 1.835876e+10

1 0.07 0.06 0.003404 20.0 1.097029e+11

2 0.08 0.04 0.028522 0.0 0.000000e+00

3 0.08 0.06 0.009494 20.0 6.023163e+10

4 0.09 0.04 0.039849 0.0 0.000000e+00

5 0.09 0.06 0.018384 14.0 1.510470e+10

6 0.10 0.04 0.051448 0.0 0.000000e+00

7 0.10 0.06 0.029543 0.0 0.000000e+00

>>> res.data()

run timestamp averange_user_health liquidations_count liquidation_volume

0 0 2023-09-29 23:30:00+00:00 0.036510 0.0 0.0

1 0 2023-09-29 23:38:34+00:00 0.036509 0.0 0.0

2 0 2023-09-29 23:47:08+00:00 0.036507 0.0 0.0

3 0 2023-09-29 23:55:42+00:00 0.036504 0.0 0.0

4 0 2023-09-30 00:04:17+00:00 0.036500 0.0 0.0

... ... ... ... ... ...

81987 7 2023-11-29 22:55:42+00:00 0.009380 0.0 0.0

81988 7 2023-11-29 23:04:17+00:00 0.009379 0.0 0.0

81989 7 2023-11-29 23:12:51+00:00 0.009379 0.0 0.0

81990 7 2023-11-29 23:21:25+00:00 0.009379 0.0 0.0

81991 7 2023-11-29 23:30:00+00:00 0.009378 0.0 0.0

81992 rows × 5 columns

>>> res.data(full=True)

loan_discount liquidation_discount run timestamp averange_user_health liquidations_count liquidation_volume

0 0.09 0.04 0 2023-09-29 23:30:00+00:00 0.059287 0.0 0.0

1 0.09 0.04 0 2023-09-29 23:38:34+00:00 0.059286 0.0 0.0

2 0.09 0.04 0 2023-09-29 23:47:08+00:00 0.059284 0.0 0.0

3 0.09 0.04 0 2023-09-29 23:55:42+00:00 0.059281 0.0 0.0

4 0.09 0.04 0 2023-09-30 00:04:17+00:00 0.059277 0.0 0.0

... ... ... ... ... ... ... ...

81987 0.12 0.06 7 2023-11-29 22:55:42+00:00 0.032402 0.0 0.0

81988 0.12 0.06 7 2023-11-29 23:04:17+00:00 0.032401 0.0 0.0

81989 0.12 0.06 7 2023-11-29 23:12:51+00:00 0.032401 0.0 0.0

81990 0.12 0.06 7 2023-11-29 23:21:25+00:00 0.032400 0.0 0.0

81991 0.12 0.06 7 2023-11-29 23:30:00+00:00 0.032400 0.0 0.0

81992 rows × 7 columns

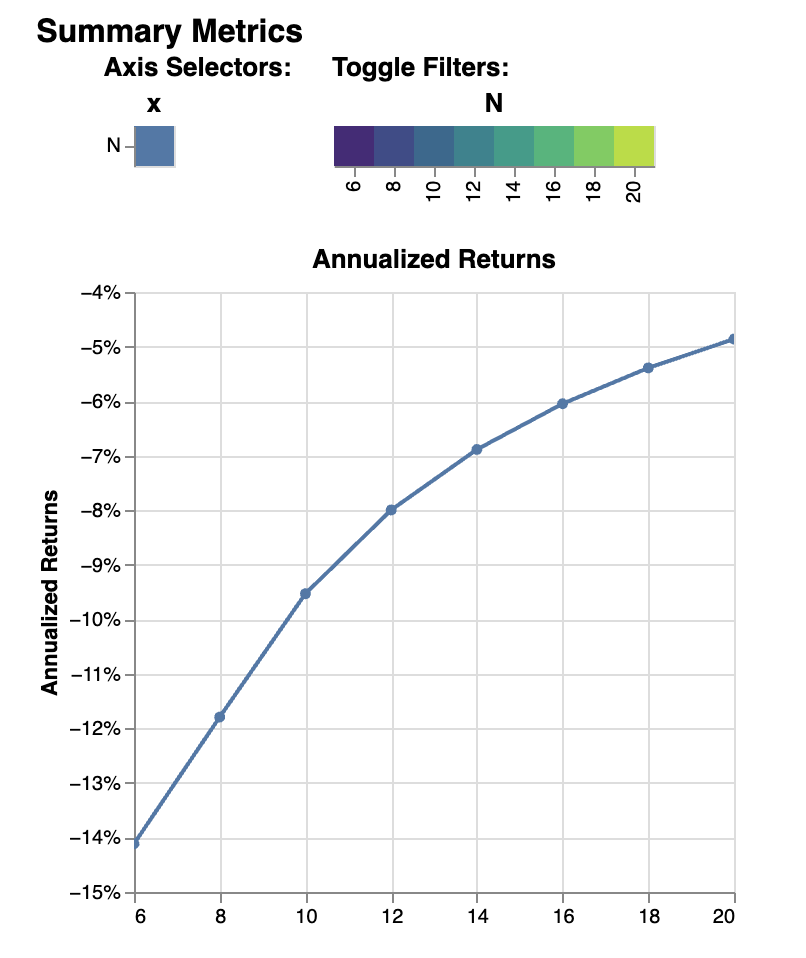

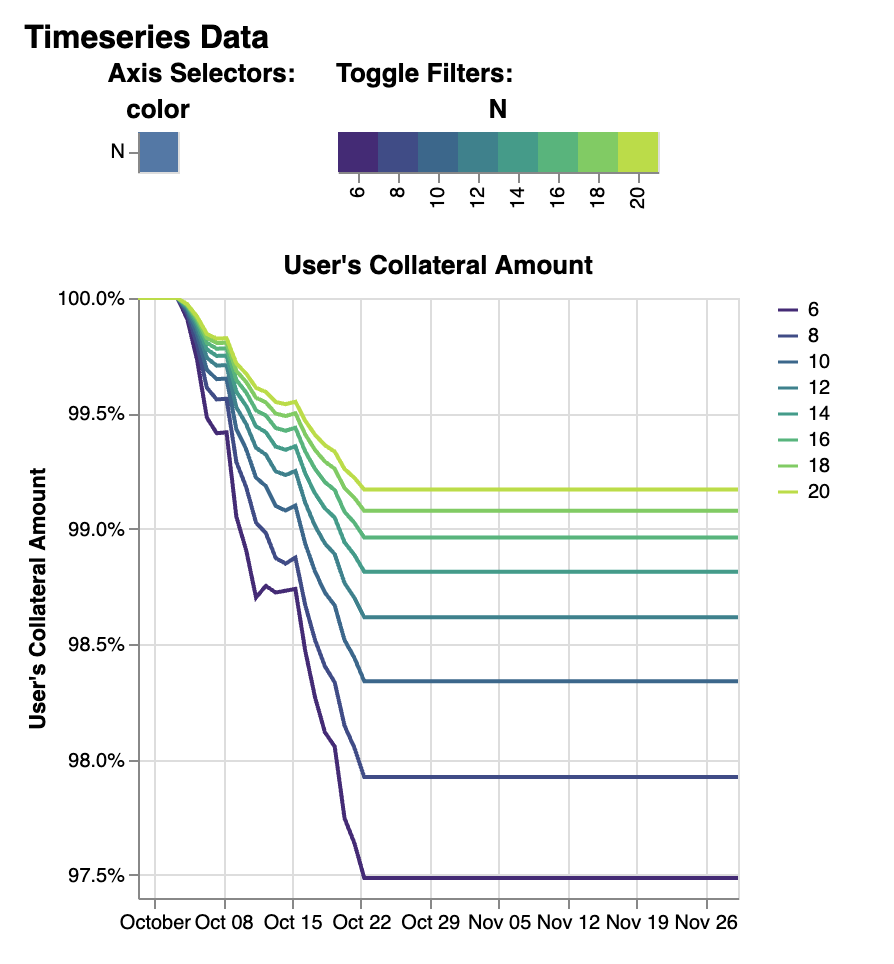

To simlate create_loan with different N parameters, use sim_mode="N":

>>> res = crvusdsim.autosim(pool="wstETH", sim_mode="N", N=[4, 6, 8, 10, 20, 40, 50])

[INFO][17:17:50][crvusdsim.pipelines.simple]-91016: Simulating mode: N

[INFO][17:17:53][curvesim.price_data.sources]-91016: Fetching CoinGecko price data...

[INFO][17:17:59][crvusdsim.templates.Strategy]-91351: [Curve.fi Stablecoin wstETH] Simulating with {'N': 8}

[INFO][17:18:01][crvusdsim.templates.Strategy]-91354: [Curve.fi Stablecoin wstETH] Simulating with {'N': 40}

[INFO][17:18:01][crvusdsim.templates.Strategy]-91349: [Curve.fi Stablecoin wstETH] Simulating with {'N': 4}

[INFO][17:18:01][crvusdsim.templates.Strategy]-91355: [Curve.fi Stablecoin wstETH] Simulating with {'N': 50}

[INFO][17:18:01][crvusdsim.templates.Strategy]-91352: [Curve.fi Stablecoin wstETH] Simulating with {'N': 10}

[INFO][17:18:01][crvusdsim.templates.Strategy]-91353: [Curve.fi Stablecoin wstETH] Simulating with {'N': 20}

[INFO][17:18:01][crvusdsim.templates.Strategy]-91350: [Curve.fi Stablecoin wstETH] Simulating with {'N': 6}

>>> res.summary()

metric user_value

stat annualized_returns

0 -0.141162

1 -0.117919

2 -0.095305

3 -0.079963

4 -0.068872

5 -0.060482

6 -0.053912

7 -0.048629

>>> res.summary(full=True)

N user_value annualized_returns

0 6 -0.141162

1 8 -0.117919

2 10 -0.095305

3 12 -0.079963

4 14 -0.068872

5 16 -0.060482

6 18 -0.053912

7 20 -0.048629

>>> res.data()

run timestamp user_value

0 0 2023-09-29 23:30:00+00:00 1.000000

1 0 2023-09-29 23:38:34+00:00 1.000000

2 0 2023-09-29 23:47:08+00:00 1.000000

3 0 2023-09-29 23:55:42+00:00 1.000000

4 0 2023-09-30 00:04:17+00:00 1.000000

... ... ... ...

81987 7 2023-11-29 22:55:42+00:00 0.991699

81988 7 2023-11-29 23:04:17+00:00 0.991699

81989 7 2023-11-29 23:12:51+00:00 0.991699

81990 7 2023-11-29 23:21:25+00:00 0.991699

81991 7 2023-11-29 23:30:00+00:00 0.991699

81992 rows x 3 columns

>>> res.data(full=True)

N run timestamp user_value

0 6 0 2023-09-29 23:30:00+00:00 1.000000

1 6 0 2023-09-29 23:38:34+00:00 1.000000

2 6 0 2023-09-29 23:47:08+00:00 1.000000

3 6 0 2023-09-29 23:55:42+00:00 1.000000

4 6 0 2023-09-30 00:04:17+00:00 1.000000

... ... ... ... ...

81987 20 7 2023-11-29 22:55:42+00:00 0.991699

81988 20 7 2023-11-29 23:04:17+00:00 0.991699

81989 20 7 2023-11-29 23:12:51+00:00 0.991699

81990 20 7 2023-11-29 23:21:25+00:00 0.991699

81991 20 7 2023-11-29 23:30:00+00:00 0.991699

81992 rows x 4 columns

Results¶

The simulation returns a SimResults object (here, res) that can plot simulation metrics or return them as DataFrames.

Plotting¶

The plot() method is used to generate and/or save plots:

#Plot results using Altair

>>> res.plot()

#Save plot results as results_pool.html

>>> res.plot(save_as="results_pool.html")

Screenshots of resulting plots (truncated):¶

sim_mode="rate"

sim_mode="pool"

sim_mode="controller"

sim_mode="N"

Metrics¶

The summary method returns metrics summarizing each simulation run:

>>> res.summary()

metric pool_value arb_profits_percent pool_volume arb_profit pool_fees

stat annualized_returns annualized_arb_profits sum sum sum

0 0.738073 -0.028339 4.828494e+09 8.927715e+06 6.569253e+07

1 0.710731 -0.024171 3.570275e+09 7.637157e+06 8.394951e+07

2 0.750342 -0.028429 4.862393e+09 9.030913e+06 6.623314e+07

3 0.739814 -0.021498 3.466717e+09 6.850344e+06 8.196935e+07

4 0.742118 -0.029061 4.860781e+09 9.280159e+06 6.617865e+07

5 0.727234 -0.023468 3.487223e+09 7.472891e+06 8.250836e+07

6 0.734865 -0.029247 4.905499e+09 9.297305e+06 6.660625e+07

7 0.731708 -0.021982 3.404420e+09 7.003415e+06 8.079451e+07

To include the parameters used in each run, use the full argument:

>>> res.summary(full=True)

A Fee pool_value annualized_returns arb_profits_percent annualized_arb_profits pool_volume sum arb_profit sum pool_fees sum

0 50 0.006 0.738073 -0.028339 4.828494e+09 8.927715e+06 6.569253e+07

1 50 0.010 0.710731 -0.024171 3.570275e+09 7.637157e+06 8.394951e+07

2 60 0.006 0.750342 -0.028429 4.862393e+09 9.030913e+06 6.623314e+07

3 60 0.010 0.739814 -0.021498 3.466717e+09 6.850344e+06 8.196935e+07

4 80 0.006 0.742118 -0.029061 4.860781e+09 9.280159e+06 6.617865e+07

5 80 0.010 0.727234 -0.023468 3.487223e+09 7.472891e+06 8.250836e+07

6 100 0.006 0.734865 -0.029247 4.905499e+09 9.297305e+06 6.660625e+07

7 100 0.010 0.731708 -0.021982 3.404420e+09 7.003415e+06 8.079451e+07

The data method returns metrics recorded at each timestamp of each run:

>>> res.data()

run timestamp pool_value arb_profits_percent pool_volume arb_profit pool_fees

0 0 2023-09-26 23:30:00+00:00 1.783265e+09 0.000000 0.0 0.0 0.0

1 0 2023-09-26 23:38:34+00:00 1.783349e+09 0.000000 0.0 0.0 0.0

2 0 2023-09-26 23:47:08+00:00 1.783433e+09 0.000000 0.0 0.0 0.0

3 0 2023-09-26 23:55:42+00:00 1.783518e+09 0.000000 0.0 0.0 0.0

4 0 2023-09-27 00:04:17+00:00 1.783602e+09 0.000000 0.0 0.0 0.0

... ... ... ... ... ... ... ...

81987 7 2023-11-26 22:55:42+00:00 1.970115e+09 -0.003708 0.0 0.0 0.0

81988 7 2023-11-26 23:04:17+00:00 1.970115e+09 -0.003708 0.0 0.0 0.0

81989 7 2023-11-26 23:12:51+00:00 1.970115e+09 -0.003708 0.0 0.0 0.0

81990 7 2023-11-26 23:21:25+00:00 1.970115e+09 -0.003708 0.0 0.0 0.0

81991 7 2023-11-26 23:30:00+00:00 1.970115e+09 -0.003708 0.0 0.0 0.0

[81992 rows × 7 columns]

The data method also accepts the full argument. However, the output may be prohibitively large:

>>> res.data(full=True)

A Fee run timestamp pool_value arb_profits_percent pool_volume arb_profit pool_fees

0 50 0.006 0 2023-09-26 23:30:00+00:00 1.783265e+09 0.000000 0.0 0.0 0.0

1 50 0.006 0 2023-09-26 23:38:34+00:00 1.783349e+09 0.000000 0.0 0.0 0.0

2 50 0.006 0 2023-09-26 23:47:08+00:00 1.783433e+09 0.000000 0.0 0.0 0.0

3 50 0.006 0 2023-09-26 23:55:42+00:00 1.783518e+09 0.000000 0.0 0.0 0.0

4 50 0.006 0 2023-09-27 00:04:17+00:00 1.783602e+09 0.000000 0.0 0.0 0.0

... ... ... ... ... ... ... ... ... ...

81987 100 0.010 7 2023-11-26 22:55:42+00:00 1.970115e+09 -0.003708 0.0 0.0 0.0

81988 100 0.010 7 2023-11-26 23:04:17+00:00 1.970115e+09 -0.003708 0.0 0.0 0.0

81989 100 0.010 7 2023-11-26 23:12:51+00:00 1.970115e+09 -0.003708 0.0 0.0 0.0

81990 100 0.010 7 2023-11-26 23:21:25+00:00 1.970115e+09 -0.003708 0.0 0.0 0.0

81991 100 0.010 7 2023-11-26 23:30:00+00:00 1.970115e+09 -0.003708 0.0 0.0 0.0

[81992 rows x 9 columns]

Fine-tuning the simulator¶

Other helpful parameters for autosim() are:

src: data source for prices and volumes. Allowed values are:

“coingecko”: CoinGecko API (free); default

“local”: local data stored in the “data” folder

ncpu: Number of cores to use.

days: Number of days to fetch data for.

end_ts: End timestamp in Unix time.

bands_strategy_class: Strategy used to initialize liquidity in LLAMMA pool bands

1:

class::crvusdsim.pool_data.metadata.BandsStrategy2: valid input:

SimpleUsersBandsStrategy,IinitYBandsStrategy,UserLoansBandsStrategy,3: or a custom strategy that inherits

class::crvusdsim.pool_data.metadata.BandsStrategy

prices_max_interval: The maximum interval for pricing data. If the time interval between twoadjacent data exceeds this value, interpolation processing will be performed automatically.

profit_threshold: Profit threshold for arbitrageurs, trades with profits below this value will not be executed

Tips¶

Pricing data¶

By default, crvUSDsim follows the pricing data module of curvesim, uses Coingecko pricing and volume data. To replace the no longer available Nomics service, we expect to onboard another data provider and also provide an option to load data files.

Note on CoinGecko Data¶

Coingecko price/volume data is computed using all trading pairs for each coin, with volume summed across all pairs. Therefore, market volume taken from CoinGecko can be much higher than that of any specific trading pair used in a simulation. This issue is largely ameloriated by our volume limiting approach, with CoinGecko results typically mirroring results from pairwise data, but it should be noted that CoinGecko data may be less reliable than more granular data for certain simulations.

Parallel processing¶

By default, crvUSDsim will use the maximum number of cores available to run

simulations. You can specify the exact number through the ncpu option.

For profiling the code, it is recommended to use ncpu=1, as common

profilers (such as cProfile) will not produce accurate results otherwise.

Errors and Exceptions¶

All exceptions that crvUSDsim explicitly raises inherit from

curvesim.exceptions.curvesimException.